Abstract

Research on oil prices has concentrated on demand and supply factors and has largely underestimated the importance of the financialization of commodities. To assess the impact of financial factors on oil prices, this article investigates the liquidity of Brazil, Russia, India, and China (BRIC) and that of a group of four developed economies (G4) consisting of the Eurozone, Japan, the United Kingdom, and the United States. An application of the single-state vector autoregressive (VAR) model to monthly data from the 1999–2020 sample period reveals that a positive shock to the liquidity of the BRIC countries leads to significant increases in real oil prices. These novel findings stem from a consideration of Markov-switching vector autoregressive (MSVAR) models, which shows that an unanticipated increase in the G4 liquidity is positively linked with real oil prices. The main findings are as follows. (1) We identify three regimes that are associated with the volatility of real oil prices and the liquidity measure, including a crisis regime that characterizes the subprime crisis and the COVID-19 pandemic. (2) Impulse response function analyses show that the impact of G4 liquidity under the crisis regime is almost twice as large as that during normal periods, while the impact of BRIC liquidity during such a crisis period is almost three times larger. (3) A shock to BRIC liquidity has a greater impact on real oil prices than a shock to the liquidity of the G4 economies. This analysis helps in assessing the importance of BRIC and G4 liquidity in relation to upsurges in the real oil prices.

Similar content being viewed by others

Introduction

The COVID-19 pandemic triggered a record one-month decline in oil prices in March 2020. The nominal price of West Texas Intermediate (WTI) at Cushing ended at US$-37 on April 20, 2020, thereby hitting negative territory for the first time.Footnote 1 Since then, oil prices have recovered somewhat; they averaged about US$30 per barrel in May 2020. Between the second and the fourth quarter of 2020, nominal oil prices continued to increase. This increase coincided with the expansionary monetary policies that were being implemented simultaneously by all major economies.

In response to the COVID-19 pandemic, central banks have taken unprecedented policy actions to ease monetary policy across the globe; therefore, M2Footnote 2 continues to increase, which causes violent fluctuations in the crude oil market. On the one hand, global liquidity has changed significantly during the pandemic.Footnote 3 On the other hand, the monetary policy responses of developed and developing countries have differed significantly. These differences motivate us to investigate the impacts of the liquidity of major developed and developing countries on oil prices. The examined developed countries are a group of four countries (G4), namely, the Eurozone, Japan, the United Kingdom, and the United States, while the examined developing countries are Brazil, Russia, India, and China (BRIC). The BRIC countries have experienced not only rapid growth in output but also a dramatic increase in monetary liquidity.Footnote 4

In this study, we examine the contributions of BRIC and G4 liquidity to real oil prices while controlling for the global short-term interest rate, global aggregate demand, and global oil supply. Following Ratti and Vespignani (2013, 2015), our liquidity variable is taken as the real M2. Our sample period covers January 1999 to December 2020;Footnote 5 thus, it includes the period of the COVID-19 outbreak. Estimating structural breaks and identifying different regimes are critical to enhancing the accuracy of estimators in a time-series analysis. Few of the existing studies on the dynamics of oil prices consider structural breaks in their model estimation (Feng et al. 2020; Kaufmann and Connelly 2020). For example, Feng et al. (2020) introduces a time-varying parameter factor-augmented VAR and captures the time-varying impact of global economic policy uncertainty on crude oil price volatility. In addition, Kaufmann and Connelly (2020) use a cointegrating relationship technique and identifies nine price regimes associated with supply and demand shocks. Our study adds to this burgeoning stream of literature by employing Markov-switching models to quantify the nonlinear effects of BRIC and G4 liquidity shocks on real oil prices.

Two streams of previous studies have examined the dynamics of oil prices. The first stream focuses on demand and supply shocks (Hamilton 2009; Kilian 2009; Kilian and Hicks 2013; Wheeler et al. 2020). Dramatic growth in the economic output of emerging markets increased the demand for crude oil and led to rapid price increases before the crisis. After the COVID-19 pandemic began, prices plummeted when the oil market was hit by an unprecedented combination of negative-demand and positive-supply shocks. The second stream argues that oil price dynamics stem from the financialization of commodities (Tang and Xiong 2012; Basak and Pavlova 2016). According to this argument, the real price of oil cannot be explained by economic fundamentals but rather is driven by the increasing financialization of oil futures markets; this view underscores the role of financial liquidity in determining the spot price of oil. We base our analysis on monetary aggregates and therefore focus on the latter perspective.

Instead of investigating monetary policy responses to commodity price shocks (Bernanke et al. 1997; Bernanke and Gertler 1999; Hammoudeh et al. 2015), we analyze the influences of monetary liquidity on oil price movements. Theoretically, the effects of global liquidity on the prices of broad categories of commodities can be explained through different channels. First, loose monetary policies lead to increases in liquidity, and the market has certain expectations about future economic growth and inflation (Barsky and Kilian, 2004). Therefore, demand increases, which leads to an increase in commodity prices. Second, some argue that the transmission mechanism of monetary policy on asset prices occurs through the supply channel (Belke et al. 2010b, 2013). Asset prices increase dramatically when the money supply increases (Gerdesmeier et al. 2010). Specifically, inelastic supply assets such as commodities are more affected by changes in global liquidity (Belke et al. 2010b). Third, following an increase in liquidity, an inventory channel might also be at work. For example, Barsky and Kilian (2002) and Frankel (2008) suggest that loose monetary conditions lead to a buildup of commodity inventories, which boosts commodity prices. Thus, oil prices are particularly influenced by monetary liquidity.

Previous studies have empirically investigated the relationship between global liquidity and commodity prices. A substantial number of papers have analyzed the impact of liquidity on the prices of broad categories of commodities (Belke et al. 2010a, b, 2013; Beckmann et al. 2014; Hammoudeh et al. 2015). Fewer papers have focused on the relationship between global liquidity and oil prices (Alquist and Kilian 2010; Anzuini et al. 2013; Ratti and Vespignani 2016; Abdel-Latif and El-Gamal 2020; Ehouman 2020), and they do not distinguish between the sources of liquidity in developed and developing economies. Ratti and Vespignani (2013, 2015) are exceptions. Based on a structural vector error correction model, these authors conclude that unanticipated positive shocks to the liquidity of Brazil, Russia, India, and China lead to significant and persistent increases in real oil prices, while this is not the case for the liquidity of developed countries. However, the authors fail to capture the different impacts of liquidity on oil prices under different regimes, as oil prices may respond to structural breaks (Noguera 2013, 2017; Feng et al. 2020; Kaufmann and Connelly 2020). Moreover, no previous studies have considered how changes in liquidity have affected oil prices differently during the COVID-19 pandemic.

The current analysis contributes to the literature in several ways. First, we contribute to the debate on the impact of liquidity on commodity prices in general. Although this issue has been extensively researched, the methods of previous research are not able to account for structural changes in commodity prices. To the best of our knowledge, this paper is the first to employ Markov-switching VAR models to measure the nonlinear effects of liquidity on real oil prices while taking into account the COVID-19 crisis. Second, while the impact of global liquidity on oil prices has been studied in the literature, the difference between the impact of BRIC liquidity and that of G4 liquidity has not been extensively studied. We follow O’Neill (2001) by placing a particular focus on the impact of BRIC monetary liquidity on real crude oil prices. Finally, this study also adds to the existing literature that explains crude oil price movements by comparing the effects of demand and supply shocks with those of liquidity shocks. Our article differs from previous studies in that its results suggest that excess liquidity leads to speculative price movements, i.e., price increases that are not justified by supply and demand fundamentals.

The remainder of the paper is structured as follows. In the section “Data and sample statistics”, we describe the variables used in the study. In the section “Methodology”, we introduce the econometric methodology. In the section “ Empirical results”, we discuss the empirical analysis. In the last section, we provide concluding remarks.

Data and sample statistics

We collect monthly data from January 1999 to December 2020. Nominal crude oil prices are measured using monthly observations of WTI from the Federal Reserve Bank of St. Louis.Footnote 6 Following Kaufmann and Connelly (2020), nominal prices are deflated (base year 1999) by the U.S. consumer price index (CPI) for all items, which is obtained from the International Monetary Fund to calculate real prices.Footnote 7

In this study, we use real M2 as a measure of the liquidity of the G4 and BRIC countries. The nominal liquidity of the G4 countries is constructed by aggregating the nominal M2 of the Eurozone, Japan, the United Kingdom, and the United States in U.S. dollars, while the liquidity of the BRIC countries is the aggregation of the M2 of Brazil, Russia, India and China in U.S. dollars. The nominal liquidity variables are also deflated (base year 1999) by the U.S. CPI. The nominal M2 data corresponding to the G4 economies, Brazil, and Russia are also from the Federal Reserve Bank of St. Louis,Footnote 8 while the nominal M2 data corresponding to India and China are from the Reserve Bank of India and the People’s Bank of China, respectively.Footnote 9 The exchange rates used to convert nominal M2 data from local currencies into U.S. dollars are retrieved from the International Financial Statistics of the International Monetary Fund (IMF).Footnote 10 Following Guo and Tanaka (2019) and Tanaka and Guo (2020), we adopt the X-13-ARIMAFootnote 11 method and adjust the real oil prices and the real M2 of the G4 and BRIC economies to eliminate the influence of seasonal fluctuations.

The monthly M2 growth rate of the G4 economies is provided in Fig. 1. It shows considerable variability within the sample period and exhibits different patterns across the examined countries. For instance, the M2 growth rate of the Eurozone changed dramatically during the Great Recession of 2007–2009 and the COVID-19 crisis. With the U.S. Federal Reserve and Congress pushing stimulus efforts to new heights, the U.S. M2 growth rate increased 16.9% at the end of April 2020 and reached an all-time high of 25.0% at the end of December 2020. Following the United States, the United Kingdom and Japan also flushed their economies with cash and bolstered their M2 supply.

Notes: The G4 economies are the Eurozone, Japan, the United Kingdom, and the United States. The X-axis denotes the years from 1999 to 2020, while the Y-axis indicates the growth rate (%) of M2. The data cover 2000:01 to 2020:12.

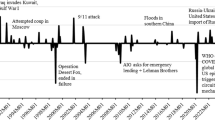

Figure 2 shows the information on the M2 growth rates of the BRIC countries. Significant fluctuations in the M2 growth rates of Brazil and Russia also occurred during the 2007–2009 Great Recession. The M2 growth rate of India also exhibited high volatility during other periods, such as 2016–2018. The M2 growth rate of Brazil peaked during the COVID-19 crisis (e.g., averaging 23.2% in 2020), while China maintained the lowest (e.g., averaging 10.3% in 2020) rate among the BRIC countries. Insights deduced from the monthly M2 growth rates of the BRIC and G4 countries may indicate regime shifts in the data series, which are examined in the analysis below.

Notes: The BRIC countries are Brazil, Russia, India, and China. The X-axis denotes the years from 1999 to 2020, while the Y-axis indicates the growth rate (%) of M2. The data cover 2000:01 to 2020:12.

Other variables included in this study are the interest rate (IR), industrial production (IP) and global production (GP) of crude oil at the global level. First, existing literature has analyzed the relationship between the U.S. interest rate and oil prices (Kilian and Vega 2011; Basistha and Kurov 2015). In the current context, however, we believe that the interaction between central bank interest rates and oil prices should be considered at the global level, especially given the rise of the BRIC countries and the new ways in which central banks are now trying to influence the economy. Second, real oil prices are also determined in markets by global demand effects. For example, Hamilton (2009) and Kilian and Hicks (2013) link increases in real oil prices to growth in emerging markets, while Belke et al. (2013) include gross domestic production (GDP) at the global level in their analysis of commodity prices. We include global industrial production (IP) in our model because this variable captures aggregate demand at the global level.Footnote 12 Third, the endogeneity of global oil production and oil production decisions is also receiving greater attention in the literature (Ratti and Vespignani, 2013, Van Robays, 2016). Following Van Robays (2016), we believe that the supply of oil affects oil prices. Thus, we control for the aggregate supply of oil by including the variable GPt, which is the average growth rate of the global production of crude oil in millions of barrels pumped per day on a monthly basis and retrieved from the U.S. Department of Energy.Footnote 13

To preserve parsimony in our framework, we construct global variables based on principal component analysis. The global IR variable is the first principal component of the G4 and BRIC countries’ IR, while global IP is the first principal component of their IP growth rates:

The variables in Eq. (1) are the discount rates of the central banks of the Euro Area, the United States, the United Kingdom, Japan, Brazil, India, Russia, and China and are retrieved from the Federal Reserve Bank of St. Louis.Footnote 14 Equation (2) is a vector that contains the IP growth rates of these countries, which are retrieved from the International Financial Statistics of the IMF.Footnote 15 To eliminate the influence of seasonal fluctuations, these series are also adjusted using the X-13-ARIMA method.

The first principal components obtained from Eqs. (1)–(2) are shown in Fig. 3. Global IR, plotted in the top panel, demonstrates a collapse in interest rates after 2008 with the onset of the subprime crisis. Global IP is shown in the middle panel. There is a severe correction between 2008 and 2009, which reflects the subprime crisis. In addition, a massive decline in industrial production can be observed starting in March 2020, as developed and emerging economies partially shut down their economies as a containment strategy for the COVID-19 pandemic. The growth rate of global oil production, plotted in the bottom panel, also shows a dramatic decrease during the COVID-19 period, consistent with the historically large production cuts agreed upon by OPEC and its partners in April 2020. The correlations between the country-specific and global factors are shown in Table 1. The correlation between global IR and country-specific IR is high for most of the G4 and BRIC countries but low for Japan and India. The correlation between global IP and country-specific IP is high for each of the G4 countries, Brazil, and India, and low for Russia and China.

Notes: The first principal components of the BRIC and G4 countries' short-term interest rates and growth rates of industrial production are taken to represent global IR and global IP, respectively. The global oil production variable is the average growth rate of global oil production in millions of barrels pumped per day on a monthly basis.

The monthly returns of oil are calculated as the first differences in the corresponding monthly logarithmic prices \({R}_{t}={{\Delta }}\ln ({P}_{t})\), where Rt is the monthly return at time t and Pt is the real oil price at time t. The liquidity measure of the BRIC countries is the first difference in the monthly logarithmic real M2 \({\rm{BRIC}}\,{\rm{Li{q}}}_{t}={{\Delta }}\ln ({\rm{BRIC}}\,M{2}_{t})\), where BRIC Liqt denotes the marginal liquidity of the BRIC countries at time t. If the overall real M2 of the BRIC countries increases at time t, then BRIC Liqt is positive. Similarly, we can construct the liquidity measure of the G4 countries as \(G4\,{\rm{Li{q}}}_{t}={{\Delta }}\ln (G4\,M{2}_{t})\), where G4 Liqt denotes the marginal liquidity of the G4 economies at time t. Therefore, vector yt is expressed as

Table 2 shows summary statistics in Panel A and correlations in Panel B. The real return on oil reaches a maximum of 58.076% and a minimum of −60.678%. The statistics in the table suggest that the return is a volatile series; this is evidenced by the high standard deviation. In addition, the median of the marginal liquidity of the G4 and BRIC countries is 0.216% and 1.122%, respectively, indicating a continuous increase in the money supply of the G4 and BRIC countries. The skewness and kurtosis of all the series do not conform to a normal distribution. Jarque-Bera tests also show that the series deviate from normality. According to Panel B, the real oil returns and marginal liquidity of the G4 and BRIC countries have positive pairwise correlations, while real oil returns are negatively correlated with global oil production.

Before constructing the econometric model, we test a stationary process for each series using the augmented Dickey–Fuller (ADF) and Phillips–Perron unit root tests. Table 3 reports the results of the unit root tests, which suggest that all the series are stationary. In particular, the results regarding the liquidity measure of the G4 and BRIC countries are significant at the 1% level, indicating that the real M2 of the G4 and BRIC countries are stationary in their first log-difference forms. In short, the data description analysis shows that these series are characterized by stationarity.

Methodology

This study aims to examine the impact of a shock to BRIC and G4 liquidity on real oil prices. We first adopt the following single-state VAR model:

where p denotes the number of lags, \({y}_{t}=({y}_{1,t},\ldots ,{y}_{N,t})^{\prime}\) is an N × 1 vector of endogenous variables, \({B}_{0}=({b}_{1,0},\ldots ,{b}_{N,0})^{\prime}\) is an N × 1 vector of intercept terms, Bj for j = 1, …, p are N × N coefficient matrices, and \({\epsilon }_{t}=({\epsilon }_{1,t},\ldots ,{\epsilon }_{N,t})^{\prime}\) is an N-dimensional error term with the same finite variance and uncorrelated with every other disturbance. Only the stationary VAR process can be represented in the form of moving averages; therefore, the stationarity of the variables in yt needs to be checked.

The endogenous variables considered in this study undergo episodes in which the behavior of the series appears to change dramatically. Such changes in the time-series process may be caused by financial crises and pandemics. Traditional regression models are unable to assess the impact of monetary liquidity on real oil prices because the time-invariant parameters cannot capture the dynamic relationships among variables of real-world data (Noguera, 2013, 2017). The literature has documented that real oil prices are unstable over time and subject to occasional regime switches. For example, Kaufmann and Connelly (2020) have identified nine price regimes that are associated with speculative bubbles and market governance.

One appealing method, namely, the Markov-switching approach, can address multiple states and include time-varying parameters. On the one hand, it is assumed that there is a probability that the variables may be in one state and can switch to another. The unobserved states are governed by an underlying Markov chain that is used to describe how the uncertainty occurs. In addition, the properties of the real data, including the means, variances, and model parameters, can change across states. These components allow Markov-switching models to fit the current data better than traditional linear models. Although Markov-switching models have been used in the analysis of stocks and bonds (Guidolin and Timmermann 2006, 2007; Ang and Timmermann 2012), the applications of this framework to energy and commodity markets are limited (Alizadeh et al. 2008, Guidolin and Pedio 2017).

The variables yt are assumed to follow a k-regimes Markov-switching process with regime-dependent intercepts, autoregressive parameters, and heteroscedasticity (MSIAH). This process is given as follows:

where St = 1, 2, …, k, \({B}_{0,{S}_{t}}\) is an N × 1 vector of regime-dependent intercepts, \({B}_{j,{S}_{t}}\) are regime-dependent coefficient matrices, and \({{{\Omega }}}_{{S}_{t}}^{\frac{1}{2}}\) is a lower triangular matrix of the Cholesky decomposition of the covariance matrix \({{{\Omega }}}_{{S}_{t}}\). St is generated by a discrete-state, homogeneous, irreducible, and ergodic first-order Markov chain with transition probabilities as follows:

where pi,j is an element of the transition matrix P with the following:

Conditional on the unobserved state, the MSIAH(k,p) in Eq. (5) reduces to the VAR (p) model in Eq. (4). To reduce the number of parameters, we also consider Markov-switching models with regime-dependent intercepts and heteroscedasticity (MSIH) as follows:

where Bj are regime-independent coefficient matrices and \({{{\Omega }}}_{{S}_{t}}^{\frac{1}{2}}\) is a lower triangular matrix of the Cholesky decomposition corresponding to the regime-dependent covariance matrix \({{{\Omega }}}_{{S}_{t}}\).

These Markov-switching models are estimated with the maximum likelihood approach, and the estimation is based on the expectation-maximization algorithm (Hamilton 1990). This algorithm includes two steps, namely, expectation and maximization. In the first round of the iteration process, we utilize the initial values of the parameters and use them in the expectation step to calculate the smoothed probabilities Pr(St = j∣yT) based on all the information in the data. The smoothed probabilities calculated in the last expectation step are the estimates of the conditional probabilities. In the maximization step, the parameters are computed as a solution to the first-order condition of the likelihood function. The estimated parameters are used to restart the expectation step and calculate new smoothed probabilities. We repeat this iterative process until convergence is reached.

Given a regime, the density function of yt conditional on the realization of this regime is assumed to be normally distributed. Following Guidolin and Pedio (2017), if the information set is available at time t−1, then the conditional density of yt is a mixture of normal distributions:

To select the appropriate model, we perform an extensive specification search using three standard information criteria, namely, the Akaike information criterion (AIC), the Hannan-Quinn information criterion (HQ), and the Schwarz information criterion (SIC). We prefer the SIC because it selects parsimonious models.

We then conduct an impulse response function analysis to quantify the effects of BRIC and G4 liquidity on real oil prices. By definition, an h-step-ahead impulse response function represents the difference between the conditional expected value of yt+h at time t when there is a liquidity shock and the conditional expected value of yt+h at time t when there is no liquidity shock. We extend this definition to a Markov-switching framework as follows:

where ηt collects the information about the states up to time t. Thus, the h-step-ahead impulse response function depends on the state. Markov-switching models are also subject to identification issues. To solve this problem, we apply Cholesky decompositions to the regime-dependent covariance matrices. For each impulse response function, we also construct a 95% confidence interval using Monte Carlo simulations, where 10,000 draws are taken from the asymptotic distribution of the coefficients.

Empirical results

Single-state VAR model selection and estimates

We begin our analysis by asking whether there is evidence of an impact of BRIC and G4 liquidity on real crude oil prices. A number of standard information criteria provide heterogeneous evidence on how many lags are appropriate for a VAR model. This number ranges from two in the case of AIC to one in the case of SIC. Considering that very parsimonious models help prevent the problem of overfitting, we choose a VAR(1) model.Footnote 16

Table 4 shows the estimates of the autoregressive parameters. Regarding real oil returns, the variables that are statistically significant are its lag term and the liquidity measure of the BRIC countries. Noticeably, the coefficient of the liquidity of the G4 economies is not statistically significant in the tests. Thus, there is relatively weak evidence of an impact of the liquidity of the G4 countries on real oil prices, which is consistent with the results of Ratti and Vespignani (2013). However, this directly contradicts the empirical evidence that most investors and policy-makers experienced from the second quarter of 2020, when real oil prices spiked as the central banks of the G4 countries announced stimulus packages, as this is clear evidence of the G4 countries’ liquidity influence. Consequently, we wonder whether extending our analysis to a Markov-switching model yields results that are consistent with the existing evidence on this topic.

Markov-switching model selection and estimates

To estimate the MSVAR models, we first have to determine the number of lags to include, the number of regimes to include, and which parameters are regime-dependent. Specifically, we consider four types of models: Markov-switching models with regime-dependent intercepts (MSIs), Markov-switching models with regime-dependent intercepts and autoregressive coefficients (MSIAs), MSIHs, and MSIAHs. Table 5 reports the model selection results. We conduct a likelihood ratio (LR) test to check if the number of states is greater than 1. The null of a single regime is always rejected. While an MSIAH(3,2) model is selected in the case of AIC, an MSIH(3,1) model is selected in the cases of HQ and the SIC (i.e., with three regimes but a time-invariant VAR matrix). To maintain parsimony, we adopt an MSIH(3,1) model.

Table 6 shows the parameters of the MSIH(3,1) model. Interestingly, the regimes are predominantly identified by the volatility of shocks in real oil returns. The regime-specific intercept coefficients differ across the regimes, suggesting that the first moments help define the states. The coefficient matrix remains constant across the regimes. On the one hand, we find significant evidence of an impact of the BRIC liquidity measure on real oil returns, consistent with the results of the single-state VAR model. Moreover, the coefficient of the variable G4 Liq (t−1) is statistically significant, suggesting that an unanticipated increase in the liquidity of the G4 economies leads to an increase in real oil prices. On the other hand, the coefficients of the variables IP (t−1) and GP (t−1) are not statistically significant, suggesting that demand and supply shocks are not the primary factors in determining real oil prices.

Moreover, regarding the BRIC liquidity variable, the coefficient of the lagged G4 liquidity variable is significant at the 5% level, evidencing a transmission of liquidity from advanced economies to emerging economies (Choi et al. 2017). However, we do not find such evidence in the opposite direction. Regarding the BRIC liquidity variable, its own lag is statistically significant. In contrast, regarding the G4 liquidity variable, its own lag is not significant. Thus, we can conclude that the money supply of the G4 economies is unpredictable and not “baked in" market prices in advance, while the BRIC countries make their monetary policies more predictable in the hope that they can curb the volatile market swings sometimes triggered by unexpected policy changes.

Identification and interpretation of regimes

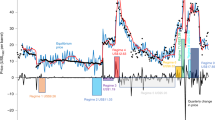

As shown in Table 7, the volatility of the variables differs substantially across the three regimes. For all the variables, volatility increases from regime 1 to regime 3. Therefore, we refer to the three regimes as the low volatility regime, the high volatility regime, and the crisis regime in the following. Regime 1, which has a low level of volatility, is the most persistent regime, and it has a stayer probability of 91.7%.Footnote 17 The probability of switching from this regime to the high volatility regime or the crisis regime is 4.2% and 4.1%, respectively. Regime 1 has a duration of 12.09 months, and Fig. 4 shows that it characterizes the period following the summer of 2009, when the subprime financial crisis was eventually addressed with force by the U.S. Federal Reserve Bank (Berge and Jordà, 2011). Moreover, regime 1 characterizes the months after June 2020, when real oil prices began to recover as nations emerged from COVID-19 pandemic lockdowns.

Notes: Regime 1 is the low volatility regime, regime 2 is the high volatility regime, and regime 3 is the crisis regime. The X-axis denotes the years from 1999 to 2020. The Y-axis denotes the probability value, which ranges from 0 to 1.

In contrast, regime 2 is a high volatility regime with a stayer probability of 91.9%. Interestingly, the probability of shifting from this regime to the crisis regime is close to 0%. As shown in the middle panel of Fig. 4, it characterizes the periods before the subprime financial crisis (apart from two isolated spikes in 2010–2011 and 2014–2015). This regime characterizes the periods when OPEC reallocated its national quotas in a way that enhanced the organization’s ability to control the supply of crude oil, pushing the price up. Under regime 2, the volatility of real oil returns is 1.5 times greater than under regime 1. In this state, real oil returns and BRIC and G4 liquidity become positively correlated, suggesting that the liquidity of the BRIC and G4 economies and real oil prices generally move in the same direction.

Finally, regime 3 represents a crisis state characterized by high volatility in real oil returns. Under regime 3, the volatility of real oil returns is 9 to 10 times higher than it is under regime 2. This regime characterizes the subprime crisis triggered by the collapse of Lehman Brothers starting in September 2008 and the COVID-19 crisis caused by the global pandemic in March 2020. It began with the onset of the subprime financial crisis, during which the returns for holding oil as a commodity also decreased (Kaufmann and Connelly 2020; Kolodziej et al. 2014). In March 2020, mitigation measures to stem the pandemic and a global recession coincided with the collapse of OPEC’s production agreement. The impact of COVID-19 was extremely severe for the oil market. There were also two isolated spikes in September 2011 and August 2015 that coincided with the European sovereign debt crisis and Chinese stock market turmoil. In August 2015, global financial markets experienced significant declines, which were accompanied by declines in the prices of commodities.

Nonlinear effects of liquidity on real oil prices

Single-state VAR and MSVAR models are useful in investigating the impacts of BRIC and G4 liquidity on real oil prices. Using a single-state VAR model, we find that a shock to the BRIC countries’ liquidity leads to a significant and persistent effect on real oil prices. Moreover, the introduction of regime switches to the MSVAR model allows us to capture the nonlinear effects of simultaneous switches of all the conditional mean functions of the variables included in the system. Using the MSVAR model, we also find significant evidence supporting an effect of the G4 liquidity measure. Obviously, a single-state VAR model is not able to detect this effect due to its static nature. To investigate the nonlinear effects of liquidity on real oil prices, we estimate the impulse response functions generated by shocks to the liquidity of the G4 and BRIC countries over an interval of 30 months. In particular, we are able to separately assess the reactions of real oil returns to these shocks when the global economy is under three different regimes.

Figure 5 plots the impulse response functions corresponding to shocks to the liquidity of the G4 and BRIC countries. We test for the presence of nonlinear impacts of G4 and BRIC liquidity shocks on real oil returns by measuring impulse response functions estimated with the MSVAR model. According to a single-state VAR model, the impact of a G4 liquidity shock is not significant. However, we find that a shock to our G4 liquidity variable leads to significant effects on real oil returns when using an MSVAR model. The introduction of regime switches into the model allows the framework to capture these nonlinear effects more accurately than a single-state VAR model could. As shown in the top and middle panels of Fig. 5, the values of the impulse response functions to shocks to the G4 liquidity measure are 0.648% and 0.812% in the low and high volatility regimes, respectively. In contrast, the value of the impulse response function under the crisis regime in the bottom panel is 1.290%, which means that the effects observed under a crisis regime are almost twice as large as those observed during other states.

Notes: The solid lines represent the estimated response functions, and the dashed lines represent the confidence intervals. IRFs stand for impulse response functions.

Using the MSVAR model, we also observe that a shock to the BRIC liquidity measure leads to significant and persistent effects on real oil returns. In particular, the values of the regime-dependent impulse response functions in the MSVAR model differ significantly in magnitude and pattern across all three regimes. The overall effects are as expected: In regime 3, which we interpret as a crisis state, the value of the impulse response function is 2.248%. In the remaining two regimes, the responses are muted, as shown in the top and middle panels of Fig. 5. The impact of a BRIC liquidity shock under the crisis regime is almost three times greater than that in the remaining states. Moreover, a shock to BRIC liquidity has a greater impact on real oil prices than a shock to the liquidity of the G4 economies. The values of the impulse response functions under the crisis regime differ substantially from those under the other regimes, highlighting the importance of including regime switches when capturing the magnitude of nonlinear effects in crisis periods.

Conclusions

In this paper, we examine the impact of BRIC and G4 liquidity on real oil prices using a single-state VAR model and a multistate MSVAR model. We also use impulse response functions to assess the response of real oil returns to a shock to the liquidity of the BRIC and G4 countries. With a single-state VAR model, we find that an unexpected increase in BRIC liquidity leads to a significant and persistent increase in real oil prices while unexpected shocks to G4 liquidity do not. However, our MSVAR model estimation suggests that a shock to G4 liquidity has a significant and persistent effect on real oil prices. The values of the regime-dependent impulse response functions differ substantially across the three regimes, i.e., the low volatility, high volatility, and crisis regimes. In particular, the impact of a G4 liquidity shock under the crisis regime is almost twice as large as that under other regimes, while the impact of a shock to the liquidity of the BRIC countries in the crisis state is almost three times larger than that of such a shock in the other two states. These results provide remarkable insight into the links between monetary policy and real oil prices and document empirical evidence of the nonlinear effects of BRIC and G4 liquidity on real oil prices.

The results highlight the dilemma that arose when major developed and emerging economies simultaneously implemented expansionary monetary policies to offset declines in their domestic production during the COVID-19 pandemic, as this caused a large monetary liquidity shock that fed into energy price inflation. Although we do not forecast the dynamics of energy prices in this study, the results suggest that further price hikes may be forthcoming given the current expansionary monetary policies of the BRIC and G4 countries. By examining the nonlinear impacts of monetary liquidity, this study also adds to the discussion on the financialization of commodities, which highlights a characteristic of financial demand in that energy and commodity prices are driven by flows of portfolio investment rather than just fundamental demand and supply factors.

Data availability

The datasets analyzed in this study are available from the Federal Reserve Bank of St. Louis: https://fred.stlouisfed.org/; the U.S. Department of Energy: https://www.eia.gov/; and the IMF’s International Financial Statistics: https://data.imf.org/. The data that support the findings of this study are available upon request from the corresponding author.

Notes

At the beginning of the COVID-19 pandemic, oil producers produced oil internationally; however, the oil ships in international waters had no customers, which contributed to the negative oil prices.

M2 is equal to cash plus checking account balances plus saving deposits. M2 is considered an indicator of money supply and a target for central bank monetary policies.

One of the first studies on the concept of global liquidity is that of Baks and Kramer (1999), who compares a variety of liquidity measures and adopts monetary growth. In addition, Rüffer and Stracca (2006) and Ratti and Vespignani (2013) discuss alternative measures of global liquidity and provide a review.

From 1999 to 2020, the M2 of the G4 economies doubled (from US$15.356 trillion to US$32.112 trillion), while the M2 of the BRIC countries increased 15-fold (from US$1.492 trillion to US$22.487 trillion). Compared to G4 countries, BRIC countries experience faster increases in liquidity.

The starting date is dictated by the creation of the European Central Bank.

Most of the relevant analyses in the literature focus on real oil price effects (Ratti and Vespignani, 2013).

The monetary aggregate L2 of India has been used as a proxy for M2. The liquidity aggregate L2 data for India are retrieved from the Reserve Bank of India; https://www.rbi.org.in/. The M2 data for China are obtained from the Money and Banking Statistics of the People’s Bank of China; http://www.pbc.gov.cn/.

X-13-ARIMA (Autoregressive Integrated Moving Average) is a popular method for seasonal adjustment.

Industrial production has the advantage of being available on a monthly basis, as opposed to GDP, which is available on a quarterly basis.

An appendix available upon request contains the results of the specification search.

The stayer probability refers to the probability that the regime will be maintained in the following month.

References

Abdel-Latif H, El-Gamal M (2020) Financial liquidity, geopolitics, and oil prices. Energy Econ 87:104,482

Alizadeh AH, Nomikos NK, Pouliasis PK (2008) A markov regime switching approach for hedging energy commodities. J Bank Financ 32(9):1970–1983

Alquist R, Kilian L (2010) What do we learn from the price of crude oil futures? J Appl Econom 25(4):539–573

Ang A, Timmermann A (2012) Regime changes and financial markets. Ann Rev Financ Econ 4(1):313–337

Anzuini A, Lombardi MJ, Paganoa P (2013) The impact of monetary policy shocks on commodity prices. Int J Cent Bank 9:119–144

Baks K, Kramer CF (1999) Global liquidity and asset prices; measurement, implications, and spillovers. Technical Report, International Monetary Fund

Barsky RB, Kilian L (2002) Do we really know that oil caused the great stagflation? A monetary alternative. In: NBER Macroeconomics Annual 2001, Vol 16. MIT Press, p 137–198

Barsky RB, Kilian L (2004) Oil and the macroeconomy since the 1970s. J Econ Perspect 18(4):115–134

Basak S, Pavlova A (2016) A model of financialization of commodities. J Finance 71(4):1511–1556

Basistha A, Kurov A (2015) The impact of monetary policy surprises on energy prices. J Futures Mark 35(1):87–103

Beckmann J, Belke A, Czudaj R (2014) Does global liquidity drive commodity prices? J Bank Financ 48:224–234

Belke A, Bordon IG, Hendricks TW (2010a) Global liquidity and commodity prices–a cointegrated VAR approach for OECD countries. Appl Financ Econ 20(3):227–242

Belke A, Orth W, Setzer R (2010b) Liquidity and the dynamic pattern of asset price adjustment: A global view. J Bank Financ 34(8):1933–1945

Belke A, Bordon IG, Volz U (2013) Effects of global liquidity on commodity and food prices. World Dev 44:31–43

Berge TJ, Jordà Ò (2011) Evaluating the classification of economic activity into recessions and expansions. Am Econ J Macroecon 3(2):246–77

Bernanke B, Gertler M (1999) Monetary policy and asset price volatility. Econ Rev (Kansas City, MO) 84(4):17

Bernanke BS, Gertler M, Watson M et al. (1997) Systematic monetary policy and the effects of oil price shocks. Brookings Pap Econ Act 1997(1):91–157

Choi WG, Kang T, Kim GY et al. (2017) Global liquidity transmission to emerging market economies, and their policy responses. J Int Econ 109:153–166

Ehouman YA (2020) Do oil-market shocks drive global liquidity? Technical Report, University of Paris Nanterre, EconomiX

Feng Y, Xu D, Failler P et al. (2020) Research on the time-varying impact of economic policy uncertainty on crude oil price fluctuation. Sustainability 12(16):6523

Frankel JA (2008) The effect of monetary policy on real commodity prices. In: Asset Prices and Monetary Policy. University of Chicago Press, pp 291–333

Gerdesmeier D, Reimers HE, Roffia B (2010) Asset price misalignments and the role of money and credit. Int Finance 13(3):377–407

Guidolin M, Pedio M (2017) Identifying and measuring the contagion channels at work in the European financial crises. J Int Financial Mark Inst Money 48:117–134

Guidolin M, Timmermann A (2006) An econometric model of nonlinear dynamics in the joint distribution of stock and bond returns. J Appl Econom 21(1):1–22

Guidolin M, Timmermann A (2007) Asset allocation under multivariate regime switching. J Econ Dyn Control 31(11):3503–3544

Guo J, Tanaka T (2019) Determinants of international price volatility transmissions: the role of self-sufficiency rates in wheat-importing countries. Palgrave Commun 5(1):1–13

Hamilton JD (1990) Analysis of time series subject to changes in regime. J Econ 45(1):39–70

Hamilton JD (2009) Causes and consequences of the oil shock of 2007-08. Brookings Papers on Economic Activity pp 215–284

Hammoudeh S, Nguyen DK, Sousa RM (2015) Us monetary policy and sectoral commodity prices. J Int Money Finance 57:61–85

Kaufmann RK, Connelly C (2020) Oil price regimes and their role in price diversions from market fundamentals. Nat Energy 5(2):141–149

Kilian L (2009) Not all oil price shocks are alike: Disentangling demand and supply shocks in the crude oil market. Am Econ Rev 99(3):1053–1069

Kilian L, Hicks B (2013) Did unexpectedly strong economic growth cause the oil price shock of 2003–2008? J Forecast 32(5):385–394

Kilian L, Vega C (2011) Do energy prices respond to us macroeconomic news? a test of the hypothesis of predetermined energy prices. Rev Econ Stat 93(2):660–671

Kolodziej M, Kaufmann RK, Kulatilaka N et al. (2014) Crude oil: Commodity or financial asset? Energy Econ 46:216–223

Newey WK, West KD (1994) Automatic lag selection in covariance matrix estimation. Rev Econ Stud 61(4):631–653

Noguera J (2013) Oil prices: Breaks and trends. Energy Econ 37:60–67

Noguera J (2017) The seven sisters versus opec: Solving the mystery of the petroleum market structure. Energy Econ 64:298–305

O’Neill J (2001) Building better global economic BRICs. Global Econ Paper 66:1–15

Ratti RA, Vespignani JL (2013) Crude oil prices and liquidity, the bric and G3 countries. Energy Econ 39:28–38

Ratti RA, Vespignani JL (2015) Commodity prices and bric and G3 liquidity: A sfavec approach. J Bank Financ 53:18–33

Ratti RA, Vespignani JL (2016) Oil prices and global factor macroeconomic variables. Energy Econ 59:198–212

Rüffer R, Stracca L (2006) What is global excess liquidity, and does it matter? Technical Report, European Central Bank

Tanaka T, Guo J (2020) International price volatility transmission and structural change: a market connectivity analysis in the beef sector. Humanit Soc Sci Commun 7(1):1–13

Tang K, Xiong W (2012) Index investment and the financialization of commodities. Financ Anal J 68(6):54–74

Van Robayrs I (2016) Macroeconomic uncertainty and oil price volatility. Oxf Bull Econ Stat 78(5):671–693

Wheeler CM, Baffes J, Kabundi AN et al. (2020) Adding fuel to the fire: Cheap oil during the COVID-19 pandemic. Technical Report, The World Bank

Author information

Authors and Affiliations

Corresponding author

Ethics declarations

Competing interests

The authors declare no competing interests.

Ethical approval

All the research was conducted in accordance with relevant guidelines and regulations. Ethical approval for this study was obtained from the Tongji University Ethics Committee.

Informed consent

This article does not contain any studies with human participants performed by any of the authors.

Additional information

Publisher’s note Springer Nature remains neutral with regard to jurisdictional claims in published maps and institutional affiliations.

Rights and permissions

Open Access This article is licensed under a Creative Commons Attribution 4.0 International License, which permits use, sharing, adaptation, distribution and reproduction in any medium or format, as long as you give appropriate credit to the original author(s) and the source, provide a link to the Creative Commons license, and indicate if changes were made. The images or other third party material in this article are included in the article’s Creative Commons license, unless indicated otherwise in a credit line to the material. If material is not included in the article’s Creative Commons license and your intended use is not permitted by statutory regulation or exceeds the permitted use, you will need to obtain permission directly from the copyright holder. To view a copy of this license, visit http://creativecommons.org/licenses/by/4.0/.

About this article

Cite this article

Zhou, Z., Zhang, X. Quantifying nonlinear effects of BRIC and G4 liquidity on oil prices. Humanit Soc Sci Commun 9, 129 (2022). https://doi.org/10.1057/s41599-022-01137-0

Received:

Accepted:

Published:

DOI: https://doi.org/10.1057/s41599-022-01137-0