Abstract

The availability of potable water is a challenging issue for many Asian countries where economies are still expanding and the population is growing. It is not difficult to observe that water scarcity will become far worse, sooner rather than later. In this study, we investigate the relationships among water indices in five Asian markets (namely China, Hong Kong, Japan, Philippines and Singapore) for the sample period 2005–2018 using the DCC-GARCH model. The empirical results confirm that volatility spillover exists among all the five water indices and there are persistent positive volatility effects. Further, we find that portfolio diversification is possible and benefits may be gained due to the contrasting correlations between pairs of these water indices. The findings of this study may be useful to academics, researchers, policymakers and major water investors worldwide in further comprehending the challenges faced by the Asian water market.

Similar content being viewed by others

Introduction

Although water is an essential commodity for survival, 2.2 billion people around the world still have no access to fresh water (United Nation Water, 2019). The amount of fresh water has been decreasing mostly due to climate change-related effects. Rainfall patterns have been changing and pollution such as those caused by floods and agricultural runoff have risen over time (Tularam and Properjohn, 2011; Tularam and Reza, 2018). It seems that climate change and its related consequences affect the long-term supply of potable water (Lancaster-Brooks, 2002; Gleick, 2006; Tularam and Reza, 2017). Potable water availability can be a challenging issue for many countries, especially some Asian countries (Roca et al., 2015; Tularam and Marchisella, 2014; Wild et al., 2007), where the economies are growing and the population is still rapidly increasing (Gleick, 1993). Therefore, the potable water-related problems may become far worse, sooner than later, in Asia (Brown et al., 2007; Tularam and Properjohn, 2011; Tularam and Marchisella, 2014).

Across Asia, approximately 783 million people are unable to readily access fresh drinking waterFootnote 1. The population growth rate in Asia and the Pacific is 1.0% (UNESCO, 2011). In Asia and the Asia Pacific about 43% of the population is currently living in urban areas and the Asia-Pacific urban proportion has risen by 29% in the past two decades, more than any other regions worldwide (UNESCO, 2011).

China is one of the most water-stressed countries in the world (Sullivan et al., 2008) with almost 22% population. More than 400 out of 663 cities in China have been suffering from water shortages, with 110 long classified as “severe” (KPMG, 2012). China’s water consumption is still on the rise and is expected to be around 1068 billion tons by 2030 (Brown et al., 2007). A large amount of investment is needed if the Chinese water industry is to perform well in the future. The current investment is probably concentrated on capital and water infrastructure only (Olstein et al., 2009). For there to be sufficient funds in the sustainment of the sector, the private sector will need to be a key player, so its participation is crucial. Not surprisingly, the water investment in the Chinese private water sector appears to be a “hot topic”, and for this reason, China has made plans to allow possible business opportunities by foreign water utilities (Lee, 2007; Hutterer, 2008).

Roca and Tularam (2012) identify China and Japan as the two significant water equity markets in Asia. In fact, the Chinese and Japanese water markets are expected to have development rates of over 8–10% in the years to come. Some statistics show that the investment profitability of Asian-based water sectors are higher than the US water industry. The Asian water sector has investment opportunities for others in that Asia has been experiencing steady growth over the past ten years.

However, in most cases, the Asian water sector has been maintained and controlled by government agencies, in that the water provision and sanitation services up to 1997 were provided by public companies. Also, in the past, there has been little appetite or interest in private investment opportunities in the Asian water industry (Grace et al., 2007). One exception is the Philippines, which is the first Asian country where the water sector is partially privatized; this was done by taking support from the World Bank and Asian Development Bank and carrying out a significant water privatization project in the world in 1997 (Brown et al., 2007; Grace et al., 2007). Singapore has also moved in this direction, and the water industry in the area has become much stronger in that the number of water companies has tripled since 2006Footnote 2. The five Asian water markets (namely, China, Hong Kong, Japan, the Philippines and Singapore) are currently experiencing growing private sector participation and this will allow further market opportunity. Essentially, the private sector can help provide financial, managerial and modern technological capacity to solve most water supply problems; that is, privatization tends to be the solution for water problems in most cases (Kessides, 2004). In sum, to address future Asian water problems, it is essential to seek larger private investments for the water industry.

In 2015, 16% of the world’s population was served by the private water companies and this is predicted to be as high as 20% in 2025 (Pinsent Masons, 2009; RobecoSAM, 2015). The increase in interest has led to a more diverse water market. The Asian water market is particularly dominated by large multinational water companies, but there are signs of financial openings for local investors, who have captured some of the water market share (Jin et al., 2019). A worldwide interest in the water market has yet to be reflected in the Asian region, notwithstanding the high forecasted growth for the region.

Globally, private water sector also requires a large amount of funds for the water investment, which has been estimated to be around US$600 billion (Roca and Tularam, 2012). The infrastructure of the Asian regions needs around US$260 billionFootnote 3. To facilitate the investing process so that large investments are possible, more in-depth knowledge of the correlations among the major Asian water-sector market indices is crucial. There is a need for water investors to better predict international portfolio diversification benefits, for example. The nature of the individual country’s water-sector market index, in fact, shows that the investment in the Asian water sector may provide high yields. This will help the private investors invest in water within their portfolios of water asset class especially if the investment allows the enhancement of diversification benefits (Jin et al., 2015a; Roca and Tularam, 2012). Diversification benefit is a desirable metric in financial portfolio calculations and aids in decision making for water investors in the process of determining whether investors may gain hedge benefits and/or profit from investing in the Asian water industry.

In terms of determining possible benefits in portfolio analysis, the use of the dynamic conditional correlation (DCC) method is common in the literature. Econometric methods such as DCC have been used to study the shock transmissions, the volatility spillover effects, diversification, and the dynamics of conditional relationships between financial assets (Peri et al., 2017). Despite the DCC-generalized autoregressive conditional heteroscedasticity (DCC-GARCH) model being the more powerful method of examining diversification and dynamics of conditional relationships, there is much less work done using this method to study the diversification benefits and dynamic relationships amongst the Asian water-sector market indices.Footnote 4

In this study, five Asian markets are investigated pertaining to the private water industry: namely China, Hong Kong, Japan, the Philippines and Singapore. The DCC-GARCH model is applied to determine correlations over time that can in turn be incorporated into portfolio modeling. In so doing, we examine the performance of the water sector in five Asian markets.

The contributions of this paper to the literature are threefold. Firstly, this is one of the few studies that investigates the dynamic relationships among the global water indices including Asian water indices. Secondly, to the best of our knowledge, no prior studies have examined the country-wise water indices in Asia with the diversification benefits of water investments. Thirdly, the results of this study would be beneficial to water-focused investors as well as to the Asian regulators in terms of containing contagion risk, thus assisting investors and institutions in making important investment decisions.

According to portfolio diversification theory, the lower (higher) the correlation of the Chinese water index with other Asian water indices, the larger (smaller) the diversification benefit to be obtained. Our results indicate that the correlations of the Chinese water index with other Asian water indices are low. Our GARCH results suggest that volatility spillover exists among the five Asian water indices. Further, DCC-GARCH results show that the Chinese water index influences the other Asian water indices. Thus, Chinese water investors now have the opportunity to diversify into other Asian countries’ water sector to achieve additional hedging benefits.

Literature review

Hedging investment funds has led to studies involving portfolio diversification implications, and the formula for variance of investment funds within a portfolio relies on variance of investments that in turn depend on correlations. Rather than using constant correlations, the use of dynamic conditional correlation relationships (correlations that can change over time) has become crucial for the calculation/prediction of the range of profits from investments. For this and other reasons, there is much research work still being done in the understanding of the relationships among equity indices, mutual funds and exchange traded funds (ETFs) including bond indices; and these in turn have become one of the main issues in hedging of funds (see, e.g., Joy et al., 1976; Longin and Solnik, 1995; Dean and Faff, 2001; Jithendranathan, 2005; Billio et al., 2006; Chiang et al., 2007; Kuper and Lestano, 2007; Asai, McAleer, 2009; Gupta and Donleavy, 2009; Li, 2009; Lafuente and Ordonez, 2009; Tularam et al., 2010; Gallali and Kilani, 2010; Gupta and Guidi, 2012; Bouri, 2013; Ahmad et al., 2014; Nagayev et al., 2016; Sclip et al., 2016; Hassan et al., 2018; Joyo and Lefen, 2019; Niyitegeka and Tewari, 2020).

By applying the DCC-GARCH model (Engle, 2002), previous studies have identified the significance and crucial importance of the dynamic conditional correlation relationships of financial markets and the potential benefits of hedging motivations especially in the international diversification case.

Unfortunately, despite its importance to water finance and investment, a smaller list of studies has investigated the risk and returns of investing in water stocks, water indices, water funds, water ETFs and water equity markets (see, e.g., Buckland and Fraser, 2000; Morana and Sawkins, 2000; Antoniou et al., 2000; Buckland and Fraser, 2001; Geman and Kanyinda, 2007; Roca and Tularam, 2012; Buckland and Williams, 2013; Buckland et al., 2015; Jin et al., 2014, 2015a, 2015b and 2019; Roca et al., 2015; Tularam and Reza, 2016; Fiorelli and Mele, 2017; Reza et al., 2017, 2018 and 2021; Vandone et al., 2018; Ibikunle and Martí‐Ballester, 2020; Piñeiro-Chousaa et al., 2020). Specifically, only four studies (Roca et al., 2013; Gilroy et al., 2013; Jin et al., 2015a; Zeneli, 2016) have investigated the correlations of water with stocks and bonds for the portfolio diversification within the water investments.

Roca et al. (2013) and Jin et al. (2015a) both use the World Water Index (WOWAX) to represent water as an investment asset. Roca et al. (2013) find that WOWAX has low correlation with MSCI World Index (MSCIWI) and Barclays Global Aggregate Index (BGAI). Hence, investors on WOWAX can gain diversification benefits from investing on MSCIWI and BGAI. Jin et al. (2015a), applying Markowitz (1952) approach, find that the WOWAX has the capacity to provide potential diversification benefits to investors on other traditional assets, i.e., MSCIWI and BGAI.

Gilroy et al. (2013) base their analysis on Palisades Global Water Index—an investable water equity index. They find that Palisades Global Water Index has high positive correlation with the MSCIW, and slightly negative correlation with bonds. But, by applying Markowitz (1952) approach, Gilroy et al. (2013) fail to note any potential diversification benefits with the Palisades Global Water Index. Zeneli (2016) selects the S-Network Global Water Index (S-Net) as a representative of water stock and finds that returns of other traditional stock are less and negatively correlated with the S-Net returns. Hence, portfolio diversification benefits are possible with the S-Net.

The study by Peri et al. (2017) is one study that examines the dynamic relationships among the water, energy and food sectors by adopting a volatility perspective using VARMA with the DCC. Their results show that correlations between the water, energy and food sectors are time-varying and that volatility spillover exists. It is noted that useful correlations exist using the DCC-GARCH model so that the appropriate diversification implications may be sought.

The dynamic nature of the DCC-GARCH model is a useful tool in determining the possibility of hedging portfolios based on diversification benefits for return calculations and thus decision making in large investments. The DCC-GARCH model, which is more parsimonious and flexible than other GARCH models such as the BEKK-GARCH model, often provides better fitting and forecasting performances (Huang et al., 2010). It also enables researchers to analyze interdependence among markets or variables by estimating the time-varying conditional correlation (Engle, 2002)—which was not available until the introduction of the DCC-GARCH model. However, studies using the DCC-GARCH method concerning the Asian water indices are lacking somewhat and therefore, our paper attempts to close this important gap in the literature.

Our paper proposes the following two testable hypotheses:

H1: The Asian water indices exhibit persistent volatility.

H2: There are dynamic conditional relationships among the Asian water indices.

Data

This study utilizes Datastream (DS) Water Index daily datasets concerning the water markets of China, Hong Kong, Japan, the Philippines and Singapore. The data are obtained from Refinitiv Datastream for the sample period from April 1, 2005 to April 30, 2018. We have selected the Chinese, Hong Kong, Japanese, Philippines and Singaporean markets not only because of the completeness of data required but also because these countries are the most important in the region in terms of size and impact. These water markets are related to financial markets in general and this helps investors engage in the private water sector in terms of indices, managed funds and ETFs. The individual water-sector market index covers private water firms, which account for 75% to 80% of the market capitalization (Roca and Tularam, 2012).

Figure 1 shows the Asian water indices’ time-series price movements. The daily returns of Asian water indices are transformed by the following formula: \({{R}}_{{{\mathrm{t}}}} = {{{\mathrm{ln}}}}\left( {{{{\mathrm{Price}}}}_{{t}}/{{{\mathrm{Price}}}}_{{{t}} - 1}} \right) \times 100\).

Price movement of five Asian water market indices, 2005–2018.

Methodology

The purpose of this study is to investigate the dynamic relationships among five Asian water indices and their volatility and returns using the DCC-GARCH model. Univariate time-series methods are thus developed in this section. Figure 2 provides a flowchart summarizing the research description and how each method answers the specific hypothesis.

Research methodology for the dynamic relationships among five Asian water indices.

A DCC model is a nonlinear combination of univariate GARCH models where the multivariate conditional variance is estimated through the univariate GARCH model for each market (Huang et al., 2010; Tularam et al., 2010). There are two steps in the estimation. First, the residuals can be obtained from the estimation of the DCC model; second, the parameters for the conditional correlation are calculated by using the transformed residuals obtained from the first step (Huang et al., 2010; Tularam et al., 2010). Following Orskaug (2009) and Tularam et al. (2010), the DCC-GARCH model, first introduced by Engle and Sheppard (2001), can be specified as:

where Ht = n × n matrix of conditional variances at time t; Dt = n × n diagonal matrix of conditional standard deviations from univariate GARCH models with \(\sqrt {\hbar _{{{{\mathrm{it}}}}}}\) on the ith diagonal and Rt = n × n conditional correlation matrix of at at time t.

By taking the substitution Ht = DtRtDt, we obtain the log-likelihood of this estimator as follows:

where εt ∼ N (0, R) is a residual, standardized by its conditional standard deviation.

We follow Orskaug (2009) and Tularam et al. (2010) to use the elements in the diagonal matrix Dt as univariate GARCH models so that we can rewrite it as follows:

for i = 1, 2,…, k with the conditions for the univariate GARCH model restrictions (non-negativity and stationarity) being imposed.

Thus, we can write the elements of Dt, the standard deviations from univariate GARCH model as follows:

Rt is the conditional correlation matrix of the standardized disturbances ∈t, i.e.,

Since Rt is a correlation matrix it is symmetric.

The elements of Ht = DtRtDt is

where ρii = 1. To ensure both of these requirements in the DCC-GARCH model are satisfied, Rt is decomposed into:

where \(\bar Q_t = Cov\left| { \in _t \in _t^T} \right| = E\left| { \in _t \in _t^T} \right|\) is the unconditional covariance matrix of the standardized errors ∈t and \(\bar Q_t\) can be estimated as:

The parameters α and β are scalars, and \(Q_t^ \ast\) is a diagonal matrix with the square root of the diagonal elements of Qt at the diagonal.

\(Q_t^ \ast\) scales the elements in Qt to ensure the second requirement, \(| {\rho _{{{{\mathrm{ijt}}}}}}| = | {\frac{{q_{{{{\mathrm{ijt}}}}}}}{{q_{{{{\mathrm{iit}}}}}q_{{{{\mathrm{ijt}}}}}}}} | \le 1\), satisfied.

We include GARCH process with normally distributed errors and follow Tularam et al.’s (2010) dynamic correlation structure, and propose a dynamic correlation model, which is:

where Q is the unconditional covariance of the standardized residuals.

Empirical results

Descriptive statistics

In Table 1, our results show that stock returns are positive in all markets except Japan. The highest mean return (0.061) is in Hong Kong, whereas Japan has the lowest mean return (−0.010), followed by the Philippines (0.042), China (0.008) and Singapore (0.007). The market with the highest risk is Japan (4.16126), followed by China (2.404), Singapore (2.207), Hong Kong (2.195) and the Philippines (1.902). These results are summarized as graphs in Fig. 3.

Mean, standard deviation, maximum, and minimum of the price movement. Note: Mean, standard deviation, maximum, and minimum results are summarized as graphs here.

Correlation matrix

Table 2 shows the correlation results amongst the five Asian water indices. The correlation matrix shows mixed results (positive or negative correlations) among China, Hong Kong, Japan, the Philippines and Singapore. It is noted that both the Hong Kong and Philippines water indices are positively correlated with the Chinese water index, whereas the Japanese and Singaporean indices are negatively correlated with the Chinese one. The Hong Kong water index is positively correlated with the Singaporean water index. However, the Japanese and Philippines water indices are negatively correlated with the Hong Kong water index. The Japanese water index is negatively correlated with the Philippines and Singapore water indices. The Philippines water index is also negatively correlated with the Singapore water index. When the correlation is somewhat low or negative, there is some scope for hedging in the market and water investors are likely to gain diversification benefits within a portfolio of investments or assets. Our analysis shows that the five Asian water indices are, at times, negatively correlated with each other. Correlation results are summarized as graphs in Fig. 4.

Correlations among the Water Index Returns of China, Hong Kong, Japan, the Philippines, and Singapore.

DCC-GARCH model

In this study, we have applied the DCC-GARCH model (Engle, 2002) to examine the return correlations between five Asian water indices (see Table 3). The Schwarz Information Criterion (SIC) is used to determine the optimal DCC-GARCH specifications. Table 3 presents the SIC results. In our case, the DCC-GARCH (1, 1) specification has the lowest SIC value and is thus adopted for the estimation.

Table 4 presents the univariate GARCH (1, 1) model estimation results for the five Asian water index returns based on Eq. (5). The estimates of volatility equations in the GARCH (1, 1) model show that all the parameters, i.e., ω—the unconditional volatility, α—the ARCH and β—the GARCH effects are positive and significant.

The coefficients for our five Asian water indices are positive and significant. The unconditional volatility (ω) of Singapore has the highest coefficient (0.401), followed by the Philippines (0.087), Hong Kong (0.075), China (0.067) and Japan (0.033). The ARCH coefficients (α) for the five Asian water indices are positive at the 1% level of significance, suggesting today’s volatility is highly related to yesterday’s innovation for all these five water indices. The GARCH coefficients (β) for the five Asian indices indicate a persistent effect, which are positive and significant for the five water indices. The ARCH and GARCH results confirm that volatility spillover exists among five water indices. These results support the hypothesis H1.

The estimation results the DCC model obtained suggest that the dynamic conditional correlations may be useful in the analyses of the water sector. The results are synthesized in Table 5 and the results support the hypothesis H2.

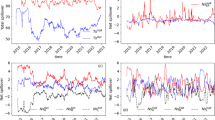

Figure 6 reports the nature of the Chinese water index and its influence in the Asian regional markets. The dynamic correlations between the water indices are rather similar to the values shown in Fig. 5. It is noted that all the dynamic correlation graphs show spikes at a similar point in time; they “build up” around 2008 and in late 2010, i.e., closely related to the ensuing global financial crisis (GFC) period. The co-movement of the Asian water indices is similar. Figure 5 shows that there is superimposition in all the DCCs of the five Asian water indices and the hedging or diversification benefits using other markets would probably be less during the GFC period.

Time-varying correlations of individual country Water Index Returns based on DCC-GARCH model.

Figures 5 and 6 both show that the Chinese and the other Asian water indices tend to fluctuate over time. However, correlation results are still within the range for benefits to be gained. Thus, hedging or portfolio diversification is possible. Figure 5 demonstrates that these five water markets provide portfolio diversification benefits to the water investors except the GFC period. Nonetheless, there may be increasing commonalities among five water indices in terms of the way water investors behave in these markets, which may bring down the diversification benefits. To obtain better risk–return trade-off, investors in the Asian water markets may include some assets in other markets into their portfolios.

Combined time-varying correlations of individual country Water Index Returns based on DCC-GARCH model.

Discussion

Our study uses multivariate GARCH model to analyze the relationships among Asian water indices including their volatility effects and returns. The correlation results obtained show that the Japanese water index is negatively correlated with the Chinese and Hong Kong water indices; the Philippines index is negatively correlated with the Hong Kong one; and the Hong Kong and Singapore water indices are negatively correlated with the Chinese, Japanese and Philippines water indices. Clearly, this finding shows that there is a possibility for hedging in the market as well as for gaining diversification benefits within a portfolio. Water investors may indeed gain international portfolio diversification benefits.

The univariate GARCH (1, 1) model results (α and β) show that the Asian water indices capture the “extremely” high level of stock return volatility. These results are in line with Reza et al. (2018). However, these results contrast with Tularam and Reza (2016) who find that there is a lower systematic risk and a positive impact on the water ETFs investment returns.

The DCC results suggest positive dynamic conditional correlations that could be used in the analysis of the Asian water sector. Similar to previous studies on other sectors (such as electricity, SRI, etc.), this study explicitly accounts for international portfolio diversification benefits with the consideration of the volatility transmission mechanism.

Conclusion

We investigate the dynamic relationships between water indices in China and other Asian markets (Hong Kong, Japan, the Philippines and Singapore) for the period 2005–2018 using the dynamic DCC-GARCH model. Our study is motivated by a need to understand the possibility of diversification and dynamic hedging or balancing of portfolios based on the types of relationships that are noted among Asian water indices, and whether Asian water indices are diversified and desirable tools for water investment.

We find that the Chinese water index has a spike in correlations with the other four Asian water indices. Although we find fluctuations in the correlations of China with the other Asian markets, the correlations remain in appropriate bands for benefits in that the Chinese market is positively correlated with the Hong Kong and the Philippines markets, while the Japanese and Singaporean markets are negatively correlated with the Chinese one, suggesting possible hedging benefits. Note that the Japanese market is negatively correlated with those in Hong Kong, the Philippines and Singapore. Also, the Philippines market is negatively correlated with the Singaporean one. Clearly, there is an avenue for water investors not only to hedge but also to diversify in the Asian water sector.

The results of our research will be helpful to academics, researchers, policymakers and major water investors worldwide. Future research may focus on other factors that drive the relationships among global and Asian water-sector markets.

Data availability

The data used in this study are available from the Datastream, which is a commercial database owned by Refinitiv. Griffith University has the license to use the data from the Refinitiv Datastream for research purpose. As affiliated researchers of Griffith University, the authors obtained the data for this study.

Notes

Due to the limited scope of this paper, the benefit analysis will not be presented here. https://www.chinawaterrisk.org/opinions/china-water-investments-3-thoughts/

References

Ahmad W, Bhanumurthy NR, Sehgal S (2014) The Eurozone crisis and its contagion effects on the European stock markets. Stud Econ Fin 31(3):325–352

Antoniou A, Barr DG, Priestley R (2000) Abnormal stock returns and public policy: the case of the UK privatised electricity and water utilities. Int J Fin Econ 5(2):93–107

Asai M, McAleer M (2009) The structure of dynamic correlations in multivariate stochastic volatility models. J Econometrics 150:182–192

Billio M, Caporin M, Gobbo M (2006) Flexible dynamic conditional correlation multivariate GARCH for asset allocation. App Financ Econ Letter 2:123–130

Bouri EI (2013) Correlation and volatility of the MENA equity markets in Turbulent Periods, and portfolio implications. Econ Bulletin 33(2):1575–1593

Brown M, Sheil DSM, Clue S (2007) Investing in Asia’s water sector: a turbulent rush through opening floodgates. venturecenter.co.in/water/pdf/ASrIA_water_report.pdf. Accessed Jun 16 2019

Buckland R, Fraser P (2000) Abnormal returns in the UK water industry since privatisation, Working Paper No. 00-10, Aberdeen Papers in Accounting, Finance and Management, University of Aberdeen, Scotland

Buckland R, Fraser P (2001) Political and regulatory risk in water utilities: beat sensitivity in the United Kingdom. J Bus Fin Account 28:877–904

Buckland R, Williams J (2013) Volatility and regulation in water supply and distribution: a post-privatization comparison of UK and US water utilities, Business School, University of Aberdeen, Aberdeen University Research Archive (AURA). http://aura.abdn.ac.uk/bitstream/2164/2968/1/WaterUtilityPaperforAURA.pdf. Accessed Jul 26 2018

Buckland R, Beecher J, Williams J (2015) Risk and regulation in water utilities: a cross-country comparison of evidence from the CAPM. J Regu Econ 47(2):117–145

Chiang TC, Jeon BN, Li H (2007) Dynamic correlation analysis of financial contagion: Evidence from Asian markets. J Int Money Fin 26:1206–1228

Dean WG, Faff RW (2001) The intertemporal relationship between market return and variance: An Australian perspective. Account Financ 41:169–196

Engle RF, Sheppard K (2001) Theoretical and empirical properties of dynamic conditional correlation multivariate GARCH. Working Paper 8554, National Bureau of Economic Research (NBER), USA. http://www.nber.org/papers/w8554. Accessed January 10 2019

Engle R (2002) Dynamic conditional correlation: a simple class of multivariate generalized autoregressive conditional heteroscedasticity models. J Bus Econ Stat 20:339–350

Fiorelli C, Mele M (2017) Water gain: as a common good becomes a financial opportunity. Int J Econ Fin 7(2):626–630

Gallali MI, Kilani B (2010) Stock markets volatility and international diversification. J Bus Stud Q1(4):21–34

Geman H, Kanyinda A (2007) Water as the next commodity. The J Alt Invest 10:23–31

Gilroy BM, Schreckenberg H, Seiler V (2013) Water as an Alternative Asset, Working Paper No. 2012-09, Center for Int Econ, Universität Paderborn, Germany. http://groups.uni-paderborn.de/fiwi/RePEc/Working%20Paper%20neutral/WP55%20-%202012-09.pdf. Accessed Mar 16 2019

Grace CPL, Karen CC, Clint KF, Serena T, Kai LT (2007). Water Privatization in Manila, Philippines Should Water be Privatized? http://www.circleofblue.org/waternews/wpcontent/uploads/2012/06/Insead_Water_Privatization_Manila_Philippines.pdf. Accessed Sept 8, 2019

Gleick P (1993) Water and conflict: Fresh water resources and international security. Int Security 18(1):79–112

Gleick PH (2006) Water and terrorism. Water Pol 8:481–503

Gupta R, Donleavy GD (2009) Benefits of diversifying investments into emerging markets with time-varying correlations: An Australian perspective. J Multi Financ Manage 19(2):160–177

Gupta R, Guidi F (2012) Cointegration relationship and time varying co-movements among Indian and Asian developed stock markets. Int Rev Financ Anal 21:10–22

Hassan MK, Paltrinieri A, Alberto DA, Miani S, Sclip A (2018) The determinants of co-movement dynamics between sukuk and conventional bonds. Quarterly Rev Econ Fin 68:73–84

Huang Y, Su W, Li X (2010) Comparison of BEKK GARCH and DCC GARCH Models: An Empirical Study. In: Cao L, Feng Y, Zhong J (eds) Data Mining and Applications6th International Conference, ADMA, Chongqing, China. pp. 99-110.

Hutterer J (2008) China’s Water Market-Opportunities for Foreign Investors. China Aktuell 2:157–177. http://www.grasshopperinvestments.com/downloads/67_Der_chinesische_Wassermart.pdf

Ibikunle G, Martí‐Ballester C (2020) Can water mutual funds aid sustainable development? J Bus Fin Account 26(1):1–18

Jin Y, Li B, Roca E, Wong V (2014) Investment returns in the water industry: a survey. Int J Water 8(2):183–199

Jin Y, Roca E, Li B, Wong V, Cheung A (2015a) Sprinkle your investment portfolio with water! Int J Water 9(1):43–59

Jin Y, Roca E, Li B, Wong V (2015b) Water as an investment: liquid yet illiquid! App Econ 48(9):731–745

Jin Y, Reza R, Li B, Roca E, Wong V (2019) Water as an investment and the impact of regulatory risk. Fin Plan Res J 5(1):55–81

Jithendranathan T (2005) What causes correlations of equity returns to change over time? A study of the US and the Russian Equity Markets. Invest Manag Financ Innov 4:69–79

Joy OM, Panton DB, Reilly FK, Martin SA (1976) Co-movement of major international equity markets. Financ Rev 11:1–20

Joyo AS, Lefen L (2019) Stock market integration of Pakistan with its trading partners: a Multivariate DCC-GARCH model approach. Sustainability 11:1–23

Kessides IN (2004) Reforming infrastructure: privatization, regulation, and competition. A World Bank policy research report, The World Bank, Washington, DC, USA. https://openlibrary.org/books/OL26393278M/Reforming_infrastructure_privatization_regulation_and_competition Accessed May 20 2019

KPMG (2012) Water in China. www.kpmg.com/cn/en/IssuesAndInsights/…/Water-in-China-201202.pdf. Accessed Mar 26 2019

Kuper GH, Lestano L (2007) Dynamic conditional correlation analysis of financial market interdependence: An application to Thailand and Indonesia. J Asian Econ 18(4):670–684

Lafuente JA, Ordonez J (2009) The effect of the EMU on short and long-run stock market dynamics: new evidence on financial integration. Int J Financ Mark Derivative 1:75–95

Lancaster-Brooks R (2002) Water terrorism: An overview of water & wastewater security problems and solutions. http://www.homelandsecurity.org/newjournal/articles/lancaster-brooks.htm. Accessed Oct 27 2018

Lee S (2007) Private sector participation in the Shanghai water sector. Water Pol 9:405–423

Li MYL (2009) Change in volatility regimes and diversification in emerging stock markets. South African J Econ 77(1):59–80

Longin F, Solnik B (1995) Is the correlation in international equity returns constant: 1960-1990? J Int Money Fin 14(1):3–26

Markowitz H (1952) Portfolio selection. J Fin 7(1):181–198

Morana C, Sawkins JW (2000) Regulatory uncertainty and share price volatility: The English and Welsh water industry’s periodic price review. J Regu Econ 17:87–100

Nagayev R, Disli M, Inghelbrecht K, Ng A (2016) On the dynamic links between commodities and Islamic equity. Energy Econ 58:125–140

Niyitegeka O, Tewari D (2020) Volatility spillovers between the European and South African foreign exchange markets. Cogent Econ Fin 8:1–17

Olstein M, Jennings J, Geist R (2009) Improving water utility capital efficiency, Water Research Foundation

Orskaug E (2009) Multivariate DCC-GARCH model-with various error distributions. Master thesis, Norwegian University of Science and Technology. https://core.ac.uk/download/pdf/52106361.pdf. Accessed Sept 8 2019

Peri M, Vandone D, Baldi L (2017) Volatility spillover between water, energy and food. Sustainability 9:1–16

Piñeiro-Chousaa J, López-Cabarcosb MA, Ribeiro-Soriano D (2020) Does investor attention influence water companies’ stock returns?. Tech Forecast Soc Change 158:1–10

Pinsent Masons (2009) Pinsent Masons water yearbook 2009–2010. Pinsent Masons LLP, London, UK

Reza R, Tularam GA, Li B (2017) An investigation into the interdependence of global water indices: a VAR analysis. App Econ 49:769–796

Reza R, Tularam GA, Li B (2018) Returns and volatility of water investments. Cogent Econ Fin 6:1–33

Reza R, Tularam GA, Li B (2021) A review of global research on private investment in the water sector. Utilities Pol 72:1–16

Robeco SAM (2015) RobecoSam Study: Water, The market of the future. 06/2015. Carbon neutral Publication. Zurich, Switzerland. https://www.robecosam.com/media/d/0/5/d05a89e800b87d21366ed8aab622c673_RobecoSAM_Water_Study_e_tcm1011-14997.pdf. Accessed May 23 2019

Roca E, Tularam GA (2012) Which way does water flow? An econometric analysis of the global price integration of water stocks. App Econ 44:2935–2944

Roca E, Li B, Wong V (2013) Water your investment portfolios. Fin Plan Magazine, The Official Publication of the Financial Planning Association of Australia 24(11):36–37

Roca E, Tularam GA, Reza R (2015) Fundamental signals of investment profitability in the global water industry. Int J Water 9:395–424

Sclip A, Alberto DA, Miani S, Andrea PA (2016) Dynamic correlations and volatility linkages between stocks and sukuk: Evidence from international markets. Rev Finan Econ 31:34–44

Sullivan C, Cohen A, Jean-Marc FJ, Santini G (2008) The rural water livelihoods index. FAO Working Paper

Tularam GA Marchisella P (2014) Water scarcity in Asia and its long-term water and border security implications for Australia. In R. M. Clark and S. Hakim (eds) Securing water wastewater systems. Springer, Switzerland. pp 189–211

Tularam GA, Properjohn M (2011) An investigation into water distribution network security: Risk and implications. Security J 4:1057–1066

Tularam GA, Reza R (2016) Water exchange traded funds: A study on idiosyncratic risk using Markov switching analysis. Cogent Econ Fin 4(1):1–12

Tularam GA, Reza R (2017) The critical importance of groundwater in coastal areas: Impact of climate change on Bangladesh freshwater resources. J Clim Change 3:59–70

Tularam GA, Reza R (2018) Subsurface Acid Sulphate Pollution and Salinity Intrusion in Coastal Groundwater Environments. In: Natarajan N, Berlin M, Vasudevan M (eds) Flow and Transport in Subsurface Environment. Springer, Singapore. pp 189–214

Tularam GA, Roca E, Wong V (2010) Investigation of socially responsible investment markets (SRI) using dynamic conditional correlation (DCC) method: Implications for diversification. J Math Stat 6:385–394

United Nations Economic and Social Commission (UNESCO) for Asia and the Pacific (2011) Statistical Yearbook for Asia and the Pacific 2011. http://www.unescap.org/stat/data/syb2011/I-People/urbanization.asp. Accessed Sept 9, 2019

United Nation Water (2019) WHO and UNICEF launch updated estimates for water, sanitation and hygiene. https://www.unwater.org/who-and-unicef-launch-updated-estimates-for-water-sanitation-and-hygiene/ Accessed Jan 20, 2020

Vandone D, Peri M, Baldi L, Tanda A (2018) The impact of energy and agriculture prices on the stock performance of the water industry. Water Res Econ 23:1–14

Wild D, Francke CJ, Menzli P, Schon U (2007) Water: a market of the future. SAM Sust Asset Manage, Zurich, Switzerland

Zeneli F (2016) Analysis of risks and investments’ opportunities in water sector. Academicus Int Scientific J 13:128–137

Author information

Authors and Affiliations

Contributions

All authors significantly contributed to the article and approved the submitted version. Contributed to the conception or design of the work: RR, GA, BL. Contributed to analysis and interpretation of data for the work: RR. Drafted the work or revised it critically for important intellectual content: RR, GA, XL, BL. Final approval of the version to be published: RR, GA, XL, BL. Agreement to be accountable for all aspects of the work in ensuring that questions related to the accuracy or integrity of any part of the work are appropriately investigated and resolved: RR, GA, XL, BL.

Corresponding author

Ethics declarations

Competing interests

The authors declare no competing interests.

Ethical approval

Not required for this study. This article does not contain any studies with human participants performed by any of the authors.

Informed consent

Not required for this study. This is because this article does not contain any studies with human participants performed by any authors.

Additional information

Publisher’s note Springer Nature remains neutral with regard to jurisdictional claims in published maps and institutional affiliations.

Rights and permissions

Open Access This article is licensed under a Creative Commons Attribution 4.0 International License, which permits use, sharing, adaptation, distribution and reproduction in any medium or format, as long as you give appropriate credit to the original author(s) and the source, provide a link to the Creative Commons license, and indicate if changes were made. The images or other third party material in this article are included in the article’s Creative Commons license, unless indicated otherwise in a credit line to the material. If material is not included in the article’s Creative Commons license and your intended use is not permitted by statutory regulation or exceeds the permitted use, you will need to obtain permission directly from the copyright holder. To view a copy of this license, visit http://creativecommons.org/licenses/by/4.0/.

About this article

Cite this article

Reza, R., Tularam, G.A., Li, X. et al. Investments in the Asian water sector: an analysis based on the DCC-GARCH model. Humanit Soc Sci Commun 9, 452 (2022). https://doi.org/10.1057/s41599-022-01470-4

Received:

Accepted:

Published:

DOI: https://doi.org/10.1057/s41599-022-01470-4